For years, the games industry was built around a comforting assumption: growth would solve almost everything.

More players would enter the market. Those players would spend more hours gaming. New hardware would unlock new audiences. Larger development budgets would produce more spectacular games, and those games would generate increasingly spectacular returns.

That logic has not disappeared entirely. But it is beginning to break.

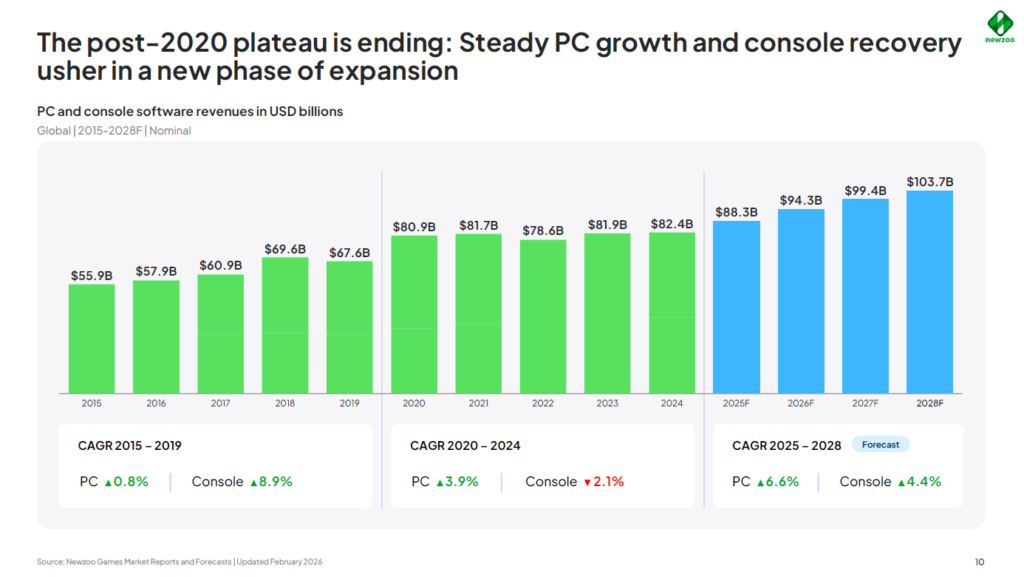

Newzoo’s 2026 PC & Console Gaming Report does not describe an industry in decline. On the contrary, PC and console software revenue is growing again after several years of stagnation. The combined market is forecast to rise from $88.3 billion in 2025 to $103.7 billion in 2028.

On the surface, that sounds like a return to normality.

Look closer, however, and the picture becomes more unsettling. Players are not spending significantly more time gaming. Console playtime is falling. New releases continue to fight over a relatively small share of total engagement. Older games dominate attention, while the cost and complexity of making new ones continue to rise.

Read another Editor’s Choice: The Illusion of Control: Why Game Rating Systems Are More Complicated Than They Look

The industry is generating more money, but it is not creating a proportionally larger supply of human attention.

That contradiction may define the next era of gaming.

Revenue growth is returning, but the old growth engine is not. The market is increasingly being pushed forward by stronger monetization, higher prices, new business models, and the redistribution of attention—not by a dramatic increase in how much time people spend playing.

Gaming is still growing. It is simply becoming much harder to win.

PC Is Becoming Gaming’s Structural Growth Engine

One of the clearest conclusions in Newzoo’s report is that PC and console gaming are no longer growing in the same way.

PC revenue is forecast to surpass console revenue by 2028. Its global player base is expected to pass one billion during the same year, compared with approximately 688 million console players.

The difference is not merely one of scale. It is a difference in the foundations supporting that growth.

PC expansion is structural. It is being driven by a widening global audience, particularly in East Asia, as well as the growing presence of Gen Z and Gen Alpha players. Steam continues to deepen its role not only as a storefront but as an ecosystem of discovery, communities, user reviews, discounts, modding, social features, and increasingly portable hardware.

The PC market does not depend on a single machine generation. It is not waiting for every player to replace the same box at roughly the same time. It can expand gradually across hardware tiers, geographic markets, price points, and types of games.

Console growth remains powerful, but more cyclical.

A major hardware launch can transform the market. A new Nintendo system, a major first-party release, a long-awaited blockbuster such as Grand Theft Auto VI, or higher subscription and software prices can generate enormous revenue. But those moments are bursts of energy rather than a permanently widening foundation.

Console remains capable of producing some of gaming’s biggest cultural and commercial events. Its users also tend to spend more per person, particularly in mature markets such as the United States, Japan, and Western Europe.

Yet its growth increasingly depends on timing: the right hardware cycle, the right exclusive, the right franchise, the right release year.

PC, by contrast, looks less explosive but more durable.

This does not mean that consoles are disappearing, nor that one platform has defeated the other. It means their economic roles are beginning to diverge. PC is becoming the industry’s broad, expanding base. Console is becoming a premium, high-spending market whose strongest years may increasingly depend on major events.

For publishers making long-term decisions, that distinction matters. A market built on steady player expansion offers different opportunities from one built on blockbusters and replacement cycles.

The Industry Is Earning More Without Winning More Time

The most important finding in the report may also be the simplest: overall playtime was effectively flat in 2025.

PC playtime increased by 3%, but that gain was offset by declines of 4% on PlayStation and 3% on Xbox. Across the three ecosystems measured, PC accounted for approximately 48% of playtime, PlayStation 34%, and Xbox 18%.

Revenue is rising. Attention is not.

That changes the meaning of competition.

A new game is not entering an expanding landscape in which every major release can find additional hours. It is entering a mostly fixed pool of time. To grow, it must take those hours from somewhere else.

Every new multiplayer game is asking players to spend less time in another multiplayer game. Every new live service is asking them to abandon existing progress, cosmetics, friends, communities, habits, and rituals.

That is an extraordinarily demanding request.

The traditional language of competition often focuses on launch windows. Publishers try to avoid releasing close to another major game. Marketing teams study crowded months, competing genres, and overlapping audiences.

But the real competition is no longer limited to the release calendar.

A game launching in 2026 is competing with titles released in 2013, 2017, 2020, and 2023. It is competing with games that have had years to accumulate content and refine their systems. It is competing against social groups that already meet every evening, inventories built over thousands of hours, and progression loops that have become part of players’ daily lives.

The fight is not simply over what people buy.

It is over what they are willing to stop playing.

Roblox Becoming Number One Is Not a Small Story

In 2025, Roblox became the most-played PC and console franchise in Newzoo’s measured markets. Its playtime grew by 52%, allowing it to overtake Fortnite and Call of Duty, whose playtime declined by 29% and 33%, respectively.

It would be easy to interpret this as another year of strong performance for Roblox. But the larger meaning is more significant.

Roblox is not simply a game in the traditional sense. It is a platform, a social environment, a distribution system, a creator economy, and an endless collection of experiences competing beneath a single identity.

Its rise reflects a broader shift in what younger audiences expect from interactive entertainment.

For many players, the attraction is not a carefully authored campaign or a single polished ruleset. It is the ability to move between experiences, play with friends, create an identity, participate in trends, and encounter something new without leaving the platform.

Minecraft and Fortnite have also moved in this direction. Each began with a clearer identity as an individual game, but gradually expanded into a larger environment containing social spaces, creative tools, collaborations, user-made experiences, and multiple forms of play.

These platforms do not merely compete for purchases. They reduce the need for players to leave.

That is a profound advantage in an attention-constrained market.

Newzoo also finds that sandbox audiences are less likely to overlap with some conventional AAA categories, particularly annual sports franchises and story-led single-player games. This challenges the assumption that younger players will inevitably “graduate” from Roblox or Minecraft into the traditional premium market.

They may not be waiting to become conventional console consumers.

They may belong to a different gaming culture with different expectations: less focused on ownership, finality, graphical prestige, or authored narrative, and more interested in participation, creativity, social identity, and continuous novelty.

For traditional publishers, the danger is not only that platform games are taking attention away from individual releases. It is that they are changing the definition of what a game is expected to provide.

New Releases Are Fighting Over 13% of Player Time

In 2025, games that were at least six years old captured 54% of total playtime. Games aged between one and five years accounted for another 33%.

New releases received only 13%.

The share available to new games has remained relatively stable in recent years. That provides a small amount of reassurance: players have not stopped trying new things.

But the scale of the challenge is difficult to ignore.

More than half of all gaming time goes to titles old enough to have outlived entire console generations, development teams, corporate strategies, and cultural trends.

For a new release, the primary competition is not only the other games arriving that month. It is Fortnite. It is Minecraft. It is Roblox. It is Grand Theft Auto V, Counter-Strike, League of Legends, World of Warcraft, and every other game that has spent years becoming part of someone’s routine.

These games carry accumulated advantages that cannot be purchased through launch marketing alone. They have content depth, player knowledge, established communities, trusted creators, cultural familiarity, and social inertia.

A new game may be technically better and still lose.

It may look more impressive and still lose.

It may receive glowing reviews and still lose, because the question facing the player is not simply, “Is this good?”

The question is, “Is this good enough to replace something I already love?”

Thousands of releases are competing over the same 13% slice of playtime. A few become major cultural events. Many receive a short burst of curiosity. Others vanish almost immediately.

This helps explain why the modern launch cycle feels so unforgiving. The market can appear excited one week and completely indifferent the next. Visibility arrives suddenly, peaks rapidly, and disappears before many studios have time to respond.

The problem is not necessarily that players reject new games. It is that they have limited room for them.

The Long Tail Is Expanding, but Discovery Is Still Cruel

Although market concentration remains intense, the report offers one encouraging development: games outside the top 20 are capturing a growing share of playtime.

By 2025, titles ranked 21 or lower accounted for approximately 42% of PC playtime, 38% on PlayStation, and 45% on Xbox.

PC showed the strongest underlying expansion. Between 2022 and 2025, playtime among games ranked below the top 20 grew by 44%.

This suggests that the market is becoming slightly less dependent on a tiny group of dominant titles. But the reasons differ across platforms.

On PC, the long tail appears to be genuinely widening. Steam’s enormous catalogue, frequent discounts, recommendation systems, user reviews, Early Access ecosystem, modding culture, and relatively low barriers to distribution allow old and niche games to remain discoverable.

A game does not need to dominate the platform to sustain a meaningful audience. It can be revived by a discount, a major update, a streamer, a mod, a sequel announcement, or a sudden cultural moment.

PlayStation remains more franchise-concentrated. Major blockbusters and established intellectual properties continue to command a larger portion of attention and spending.

Xbox has broader playtime distribution, helped by Game Pass. Players can experiment with more titles because the immediate cost of trying them is lower. However, Newzoo suggests that this often redistributes existing Xbox playtime rather than dramatically increasing the total hours spent on the platform.

The long tail is therefore becoming healthier, but it is not becoming easy.

Being outside the top 20 is increasingly survivable. Being invisible remains effortless.

For smaller studios, that is both hopeful and sobering. There is more room to build a durable audience without becoming a global phenomenon. Yet discovery remains a constant responsibility rather than a launch-week task.

A good game can survive quietly. It cannot survive if nobody knows it exists.

Longevity Matters More Than Launch-Week Spectacle

The report’s analysis of games that endure beyond the top tier points toward a different model of success.

The strongest long-term performers tend to be premium games with meaningful progression, substantial catalogue value, and strong RPG or adventure elements. They are not always the games with the loudest launches. They are the games that continue giving players reasons to return, recommend, purchase expansions, or explore earlier entries.

This distinction is essential.

A game can be viral without being durable. It can generate millions of views, dominate social media, attract a huge opening-week audience, and still disappear quickly.

Launch momentum is an event. Longevity is a system.

Durable games often create multiple forms of value over time. Progression gives players an unfinished journey. Replayability gives them a reason to begin again. Expansions renew attention. Updates create fresh conversation. A strong back catalogue allows one successful title to lift the commercial performance of an entire franchise.

The result is that a focused premium game with a strong identity may now be a healthier business than an enormous live-service project designed for a hypothetical mass audience.

The industry has spent years chasing recurring revenue. In doing so, it has often underestimated the durability of ownership, craftsmanship, and complete experiences.

Players may not need every game to become a permanent service. Sometimes they want to buy something distinctive, love it deeply, finish it, recommend it, and return when there is something meaningful to return to.

That relationship can be commercially powerful precisely because it does not begin by demanding endless commitment.

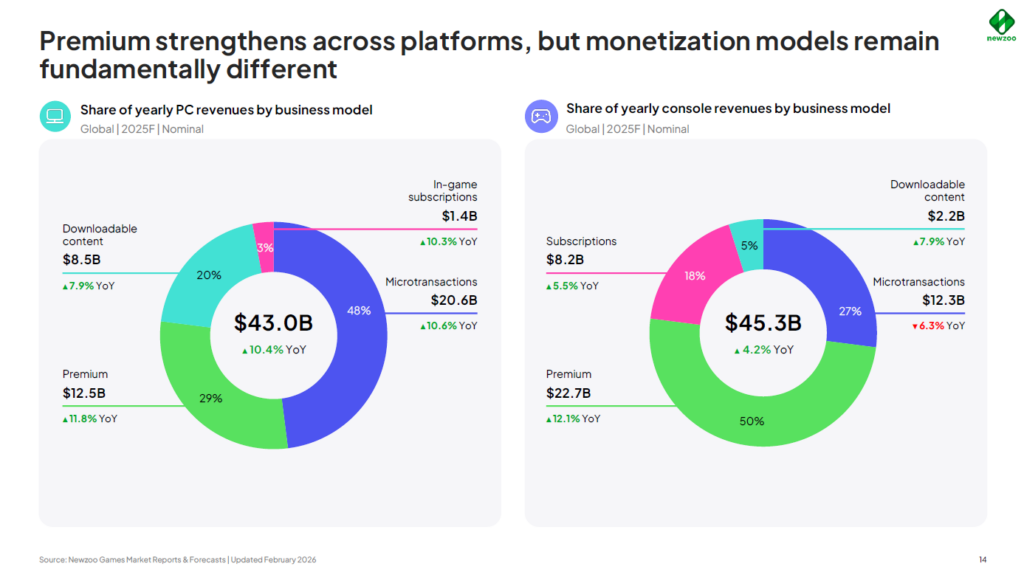

Premium Games Are Carrying Revenue Growth

In 2025, premium revenue increased by 11.8% on PC and 12.1% on console. At the same time, console microtransaction revenue declined by 6.3%.

That is not evidence that free-to-play has collapsed. PC continues to monetize free-to-play successfully, and its microtransaction revenue remains substantial. But the platform differences are becoming clearer.

PC can sustain several economic models simultaneously. It supports premium blockbusters, low-cost independent games, Early Access, free-to-play titles, downloadable content, subscriptions, mods, and enormous back catalogues.

Console remains more dependent on premium spending. Free-to-play engagement still exists, but its revenue is weakening more rapidly than engagement itself.

This creates a difficult environment for publishers still treating live service as the default answer to every commercial problem.

Free-to-play is not merely a pricing decision. It requires a constant content pipeline, sophisticated retention systems, a functioning in-game economy, community management, technical reliability, long-term acquisition spending, and enough scale to support all of those operations.

When player time is not expanding, every new free-to-play game enters a contest against the most entrenched products in the industry.

The failure rate is not surprising. What is surprising is how often companies continue to treat the model as a shortcut to growth.

Free-to-play can be extraordinarily profitable. But it is becoming less forgiving, particularly on consoles. It is no longer enough to remove the purchase price and wait for an audience to arrive.

The Most Interesting Price Is Between $30 and $50

One of the most useful commercial findings in the report is the growth of premium games priced below the traditional blockbuster tier.

The $30–$50 segment is the fastest-growing premium price band across platforms. Games below $30 are also performing well on PC, particularly when independent titles break through.

Games priced above $50 still dominate console premium revenue. In 2025, they represented approximately 79% of PlayStation premium revenue and 76% on Xbox. But their share is declining as lower-priced games gain ground.

This does not mean that the $70 blockbuster is disappearing. The largest franchises can still justify premium pricing through scale, reputation, production value, and demand.

The more important change is that the market is creating room for another proposition.

A game does not need to imitate the scope of the largest releases. It can offer a clearer, more focused experience at a price that feels proportionate to its ambition.

That balance may explain the appeal of games such as Clair Obscur: Expedition 33, Helldivers 2, Schedule I, and many successful independent titles. They do not necessarily promise everything. They promise something distinct.

For players, that can feel refreshing. For developers, it can create a more realistic relationship between budget, price, audience size, and expected return.

A $200 million game must appeal to an enormous number of people. A smaller game can afford to have a personality.

That may be one of the most important advantages in today’s market.

The Old AAA Formula Is Becoming a Liability

For much of modern gaming history, the industry followed a familiar escalation.

Spend more. Build more. Increase the map size. Extend the campaign. Add more modes. Hire more people. Market the game more aggressively. Create an event large enough that players cannot ignore it.

That formula worked when the audience, available playtime, and commercial ceiling all appeared to be expanding together.

Now, the same scale can become dangerous.

The larger the budget, the more players a game must reach. The longer the development cycle, the greater the risk that tastes, technology, or market conditions will change before release. The more generic the design, the harder it becomes to inspire genuine attachment.

An expensive game cannot afford to be merely good. It must become an event.

But events are temporary, and player habits are stubborn.

This creates a particularly dangerous middle ground: the large, polished, relatively conventional AAA release that is too expensive to succeed as a niche product but not distinctive enough to pull players away from established games.

It may have excellent visuals, competent mechanics, a vast world, and an enormous marketing campaign. Yet it arrives without a compelling answer to the most important question:

Why should anyone leave the games they already play?

The New Logic of Success

The old industry logic could be summarized simply:

Spend more money, make a bigger game, launch it harder, and reach more players.

The emerging logic is different:

Find a distinct audience. Give the game a clear identity. Price it intelligently. Build meaningful progression. Respect the player’s time. Create reasons to return without assuming they will stay forever.

The likely winners are increasingly falling into three groups.

The first are platform ecosystems such as Roblox, Fortnite, and Minecraft. They survive by containing many experiences, communities, and forms of expression inside a single environment.

The second are deep evergreen games such as Counter-Strike, League of Legends, Grand Theft Auto, and World of Warcraft. They have accumulated years of content, player investment, knowledge, identity, and social attachment.

The third are focused premium games: titles with controlled budgets, strong creative identities, meaningful progression, intelligent pricing, and enough cultural relevance to break through without needing to dominate the entire market.

These models are very different, but they share one quality.

They understand exactly why the player should care.

That clarity may now matter more than scale.

Growth Without Abundance

The games industry is not shrinking. But it is losing the comfort of abundance.

There may be more revenue, but there is not much more time. There may be more players, but their attention is increasingly concentrated inside ecosystems designed to retain them indefinitely. There may be more ways to publish a game, but there are also more games competing to be noticed.

This is not the end of growth. It is the end of effortless assumptions about where growth will come from.

The next era will reward companies that understand the difference between reach and attachment, between launch visibility and long-term value, between a large audience in theory and a real community in practice.

Players do not owe a game their time simply because it was expensive to create.

They do not owe a publisher loyalty because a franchise was once important.

They do not owe a live service ten years of engagement because its business plan requires it.

Attention must be earned, and then earned again.

That reality may be painful for an industry accustomed to solving problems with larger budgets. But it may also lead to better games: games with clearer identities, more disciplined scope, fairer prices, and a more honest understanding of what players actually want.

Gaming is growing again.

The uncomfortable truth is that growth will no longer rescue every game built to chase it.